Q&A-Resource Guide Offers Academy’s Health Expertise

A new Health Practice Council (HPC) suite of publications-Health Insurance Market Dynamics: A Resource Guide-offers insight on how aspects of health insurance markets influence each other. Developed by the HPC’s Individual and Small Group Markets (ISGM), Medicaid, and Active Benefits committees, the guide includes:

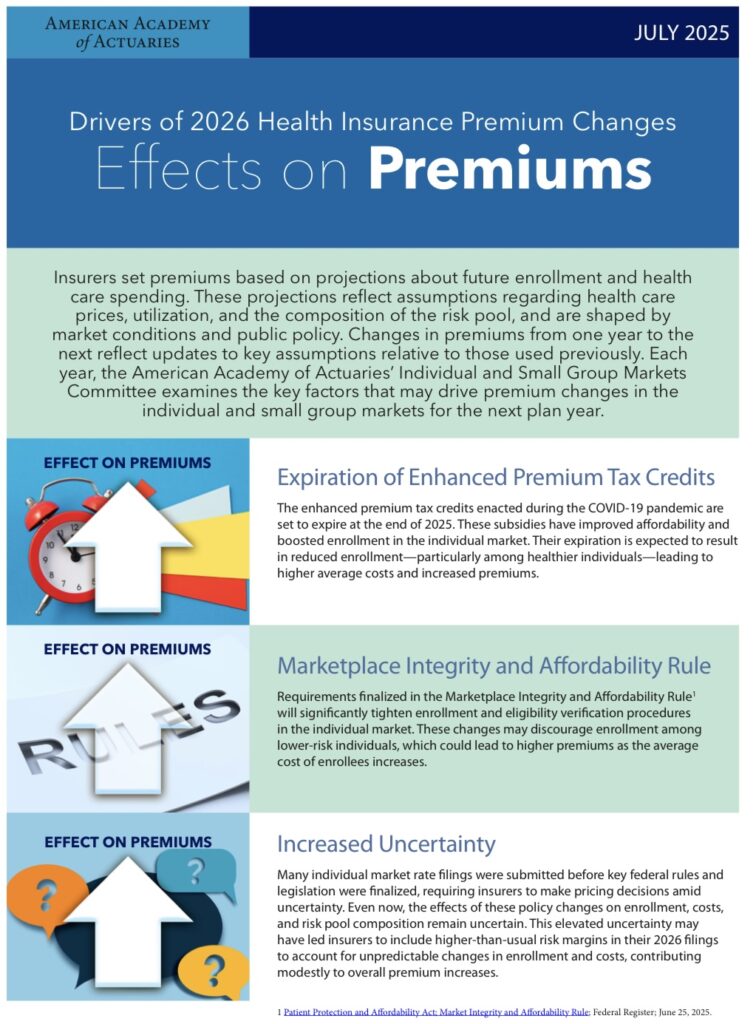

• An issue brief, Drivers of 2026 Premium Changes, and accompanying infographic.

• An illustrative premium-rate development timeline.

• Two discussion briefs-Strategies to Achieve Market Stability in the Individual Health Insurance Market and The Interconnectedness of Health Coverage Sources for the Under-65 Population.

The guide offers actuarially grounded resources, reflecting how the stability and enrollment of the individual and small group markets (also known as Affordable Care Act, or ACA, markets), large-group employer-sponsored health plans, and state Medicaid programs are interrelated and interdependent.

“Changes such as the expiration of enhanced premium tax credits or increased availability of non-compliant plans could destabilize the market by increasing adverse selection and raising premiums,” Academy Senior Health Fellow Cori Uccello said in the Academy’s news release on the new resources.

To walk through its implications, HealthCheck did a Q&A with Uccello on the resource guide.

Editor’s note: The Q&A was conducted in mid-August-any subsequent legislative or regulatory changes (or court decisions) could affect 2026 premium rates and market stability.

For most of the spring and early summer, Congress worked on the major budget reconciliation package, which was ultimately signed into law on July 4. What are some of the key health provisions?

The law includes several provisions affecting both the ACA marketplaces and Medicaid. For the individual market, it tightens subsidy eligibility verification starting in 2027-though CMS [the Centers for Medicare & Medicaid Services] has finalized rules applying similar requirements for 2026. It also deems all bronze and catastrophic plans HSA [health savings account]-qualified, expanding tax-advantaged coverage options. Notably, the law does not extend the enhanced premium tax credits, which are still set to expire at the end of 2025, nor does it provide funding for cost-sharing reduction payments-meaning “silver loading” will continue for the time being.

On the Medicaid side, the law imposes work requirements for most non-disabled, non-elderly adults in expansion populations and mandates semiannual income and residency checks. States must implement these provisions by the end of 2026, though some may delay until 2028 with federal approval. The law also phases down the enhanced federal match for expansion enrollees starting in 2026, gradually reducing it from 90% to 85% by 2030. Additional provisions-including tighter limits on provider taxes and caps on state-directed payments-also take effect in 2026. A new $50 billion rural hospital fund begins rolling out that same year. Together, these changes have broad implications for state budgets, provider payments, and coverage continuity.

How will these provisions impact stability in the individual market?

As outlined in our market stability discussion paper, a stable individual market relies on broad enrollment, a balanced risk pool, and a predictable policy environment. Current policies that support stability include premium and cost-sharing subsidies that make coverage more affordable, single risk pool requirements that spread risk, and uniform rules and risk adjustment that help ensure fair competition among insurers.

However, upcoming policy changes could undermine this stability. Stricter subsidy eligibility verification-finalized in the 2026 Marketplace Integrity and Affordability Rule and continued via the new law beginning in 2027-may reduce enrollment. Individuals with health care needs are more likely to navigate added administrative hurdles, while healthier individuals may be more likely to forgo coverage. If the enhanced premium tax credits expire as scheduled at the end of 2025, coverage could also become less affordable for millions-particularly for healthier individuals who are more price-sensitive and more likely to drop coverage when costs rise. These changes could lead to enrollment declines, a deterioration of the risk pool, and-as discussed below-higher premiums. If market conditions worsen significantly, some insurers may reconsider their participation.

Editor’s note: On Aug. 22, a federal district court issued a stay on several provisions in the Marketplace Integrity and Affordability Rule. The Trump administration is appealing the ruling on one of the provisions, regarding actuarial value. At this stage, not all of the stricter eligibility requirements are going into effect for 2026.

The paper on market interconnectedness highlights how changes in one coverage source can ripple into others. How might the Medicaid changes affect the individual market?

Stricter Medicaid eligibility requirements-such as more frequent income checks-could lead to coverage losses and shifts into the individual market, where many affected individuals may qualify for subsidized coverage. If those making the transition are relatively healthy, their entry could help stabilize premiums; if they have greater health care needs, premiums may rise. The impact will depend on the health profile of those entering the market compared to the current risk pool mix.

Other changes, such as Medicaid work requirements, may have different implications. Individuals who lose Medicaid coverage because they don’t meet work requirements are not eligible for subsidized coverage through the marketplaces, leaving them with few affordable alternatives. As a result, they may be more likely to become uninsured. In addition, how states respond to reduced federal Medicaid funding-such as by narrowing eligibility or reducing benefits-could further influence both uninsurance rates and enrollment in the individual market.

What are the main drivers behind expected premium increases for 2026?

As detailed in our issue brief and infographic on 2026 premium drivers, premiums are expected to rise due to a combination of medical cost growth and changes in the risk pool. Medical trend continues to rise, driven by inflation, increased drug spending-particularly from new high-cost therapies-and sustained demand for behavioral health services.

On the risk-pool side, several dynamics are contributing to upward pressure. The expiration of enhanced premium tax credits and stricter enrollment verification requirements are expected to reduce enrollment, especially among healthier individuals, worsening the average risk profile. (Editor’s note: As noted above, not all of those requirements are going into effect for 2026.)

The Medicaid unwinding may also affect premiums, depending on the relative health of those transitioning to the individual market-some states may see healthier enrollees, others less so. In the small group market, steady declines continue as employers shift to self-funded or level-funded options, leaving higher-cost groups in the fully insured pool. The use of account-based plans like ICHRAs [individual coverage health reimbursement arrangements] may also shift workers into the individual market, with varying effects depending on the health status of those making the move.

State and local factors-such as insurer competition and regulatory changes-also play a role. And when the effects of policy shifts are uncertain, insurers may increase risk margins as a precaution.

As the premium development timeline shows, the rate-setting process begins long before open enrollment. If Congress were to act to extend enhanced subsidies, could that still be reflected in 2026 premiums?

Yes-if action is taken quickly. Insurers can revise and resubmit their rates, but the process takes time. Depending on the complexity of the policy change, updates could take two to six weeks (or more) for submission and review. Swift legislative action would be necessary for any changes to be incorporated into 2026 premiums. Believe it or not, development of 2027 premiums begins around this month, in September.

Webinar Examines Premium Drivers-The ISGM Committee hosted an Aug. 5 webinar that examined the premium rate drivers issue brief, as well as the discussion brief highlighting the degree of interconnectedness between the insurance markets and how public policy changes and market dynamics may affect market stability and costs. Catch a replay on the Academy’s YouTube page.

Medicare Issue Brief Released; Webinar Set for Sept. 9

The Medicare Committee released an issue brief, Medicare’s Financial Condition: Beyond Actuarial Balance, examining the findings of the 2025 Medicare Trustees Report with respect to program solvency and sustainability. Financing challenges, including inadequate income and increased spending, led the trustees to conclude that the Hospital Insurance Trust Fund is projected to be depleted by 2033, three years earlier than projected in 2024’s report.

Sept. 9 Webinar-The Health Practice Council is holding a webinar on Sept. 9, Medicare: Where Are We Now? And, Where Are We Headed? It will offer a deep dive into the annual Medicare Trustees Report, with Academy Medicare Committee Chairperson Derek Skoog summarizing and providing insights on the report’s findings. Attendees will also hear from Carrie Graham, a research professor and Director of the Medicare Policy Initiative from the Georgetown Center on Health Insurance Reforms; and Frank McStay, the assistant research director for the Duke-Margolis Institute for Health Policy’s Medicare Accountable Care Transformation. Continuing education credit is available for this live webinar. Register today.

Academy Presents at NAIC Summer Meeting

Academy volunteers and staff offered public comments at the NAIC Summer National Meeting in Minneapolis in mid-August, covering health and other public policy practice areas and professionalism issues.

Health Vice President Annette James presented to the Health Actuarial (B) Task Force (HATF) on “2026 Health Insurance Premiums in Focus: Policy Changes and Impacts on Market Stability,” and Public Policy State Outreach Director Katie Dzurec gave an update on Health Practice Council (HPC) activities.

Dzurec also offered comments to the Risk-Based Capital Model Governance (EX) Task Force on their proposed framework and principles document, speaking on behalf of the HPC, Life Practice Council, Casualty Practice Council, and Risk Management and Financial Reporting Council.

Video recap, blog post-More details of the Academy’s engagement in Minneapolis are available in an Actuarially Sound blog post, and the regular post-meeting recap is available to watch on the Academy’s YouTube page.

Academy Leaders Present at ARC 2025

Academy leaders, including President Darrell Knapp and Health Vice President Annette James, spoke at the Actuarial Research Conference (ARC 2025), held July 29-Aug. 1 in Toronto.

“The Academy itself is a consumer, producer, and promoter of research across all actuarial practice areas,” Knapp said in his opening-session remarks. “Research helps actuaries and the Academy communicate objective insights and new information in their work and on issues ranging from climate change’s impact on financial security systems to the role of bias in assessing financial risk.”

Knapp introduced James, who spoke in a July 30 session on “From Code to Culture: Living Professionalism Every Day.”

Research Committee Chairperson Grace Lattyak also presented the Academy’s third annual Award for Research to Xi Xin, a Ph.D. candidate at the University of New South Wales in Australia.

The ARC 2025 program included speakers from the Canadian Institute of Actuaries (CIA), the Casualty Actuarial Society (CAS), and other actuarial organizations. The Academy, along with the CIA, CAS, and the Society of Actuaries, were ARC 2025 sponsors.

HPC Presents to CCIIO

Health Vice President Annette James, Individual and Small Group Markets (ISGM) Committee Vice Chairperson Tammy Tomczyk, and Senior Health Fellow Cori Uccello presented June 11 to the Centers for Medicare & Medicaid Services’ (CMS) Center for Consumer Information and Insurance Oversight (CCIIO) on “Public Policy Activities Related to the Individual and Small Group Markets.”

The presentation covered the Health Practice Council’s (HPC) priorities, the ISGM Committee’s recent and upcoming publications, which included a discussion of potential 2026 premium drivers and the illustrative 2026 premium rate development timeline from the Health Insurance Market Dynamics Resource Guide.

Board Selection Process Underway; Includes Two Health Volunteers

The Academy’s member-selected process kicked off Sept. 3 and runs through Sept. 17. This year’s three candidates include two health volunteers, Ron Ogborne and Becky Sheppard, along with retirement volunteer Joseph Hicks.

Members should have received an Aug. 22 email from Intelliscan, the Academy’s selection-process vendor, from Academy@intelliscanvotes.com. The candidates will serve three-year terms beginning in November, with the Academy’s leadership transition.

- Ron Ogborne is a member of the Health Practice Council (HPC) and past chairperson of the LTC Medicaid Subcommittee. He is a member of the Health Care Delivery Committee and has served on the Medicaid Committee, Solvency Committee, and Climate Change Joint Committee. Ogborne was featured in an Academy Member Spotlight.

- Becky Sheppard is a member of the HPC and chairs the Health Equity Committee. She is also a member of the Board’s Diversity, Equity & Inclusion Committee, the Research Committee, and the Actuarial Standards Board’s ASOP No. 41 Task Force. Sheppard received a 2024 Outstanding Volunteerism Award for her efforts in the health area, and was featured in Actuary Voices (April 2024).

As a reminder, the Academy’s selection process is not a competitive election. Instead, the Nominating Committee reviews the member-nominated candidates based on Board needs, and puts forward three candidates for members to confirm. Those three member-selected directors will join the full slate in November.

For more and a look at the 2025-2026 Board of Directors prospective slate, visit the Board Selection Center.

Issue Brief Examines Post-Pandemic LTC Insurance

A health issue brief, The Impact of COVID-19 on Long-Term Care Insurance Experience-2025, spotlights the impact of COVID-19 on long-term care insurance since the start of the pandemic five years ago. It is a follow-up to a January 2021 issue brief that addressed a broad array of issues and questions impacting, or potentially impacting, the LTCI market.

Key points include:

- Several areas of uncertainty may continue to exist, including long-term morbidity and mortality effects of long-COVID; availability of related data; long-lasting effects of mRNA modifications; and capital market uncertainty.

- During the pandemic, many LTCI carriers observed increased mortality, particularly disabled life mortality.

- Actuarial experience from the core years of the pandemic (2020-2022) is now measurable and the short-term economic volatility and disruptions have subsided, although insurance companies may use varying approaches to developing assumptions, based on the data from this period.

Highlights From

HealthCheck

Prefer to watch your news? Check out this “Highlights From HealthCheck” video for a quick recap of what you need to know.

Health News in Brief

The Health Equity Committee presented at the Society of Actuaries’ (SOA) 2025 virtual Health Meeting in Dallas. Committee member Maggie Ruzicka moderated the session, which included a discussion on health equity concerns with respect to non-traditional benefits, such as food as medicine, in a standard benefits package.

The Academy attended the National Conference of State Legislatures’ 2025 Legislative Summit in Boston, participating in meetings with state legislators, state legislative staff, and other stakeholders on health and other practice-area issues. This year’s 50th anniversary summit included a special focus on issues related to AI and cybersecurity, extreme weather events, and insurance affordability.

The ISGM Committee sent comments to Senate leadership as they developed their budget reconciliation legislation when H.R. 1 was under consideration.

Academy in the News

The HPC’s recently released package of health policy resources on 2026 ACA premiums, market stability, and interconnected markets garnered coverage in several outlets, with comments from Uccello in Insurance News Net and Inside Health Policy, and from HPC member Susan Pantely in Bloomberg Law.

ISGM Committee Vice Chairperson Tammy Tomczyk addressed the role of state regulation and factors health insurers may consider in covering vaccines in a STAT News article about recent changes in the Advisory Committee on Immunization Practices.

Senior Health Fellow Cori Uccello authored a Health Affairs Forefront article examining how tradeoffs between premiums and cost sharing affect health insurance affordability, who ultimately bears the cost of care, and how different policy options could shift that balance.

Uccello co-authored a Health Affairs article with Gretchen Jacobson exploring why Medicare Advantage defied expectations with rapid growth after enactment of the ACA. The article also explores reform options to further improve Medicare Advantage for beneficiaries.

The Wall Street Journal quoted Uccello on the impact of changes in federal policy in a story about insurers’ proposed 2026 ACA premium rate increases. In a separate story, Uccello noted new, expensive treatments as a factor in cost pressures facing health insurers.

Uccello spoke to the impacts of prospective risk pool deterioration in ACA markets in a Politico Pro story on emerging challenges facing health insurers. In a separate story, she discussed potential implications of federal policy changes for employer-funded individual coverage health reimbursement arrangements.

The Northwest Arkansas Democrat-Gazette cited the Academy to help readers understand actuarial soundness in a story on individual market proposed rate increases in the state.

Insurance News Net reported on the Academy’s recent issue brief on 2026 premium drivers.

A Commonwealth Fund blog on the budget reconciliation bill and how it will affect health plan marketplaces, access, and affordability cited the HPC’s comment letters to the U.S. House Budget Committee and U.S. Senate leadership.

Legislative/Regulatory Activity

Federal

President Trump on July 4 signed H.R. 1, also known as the One Big Beautiful Bill Act. The new law directly impacts Medicaid, long-term care (LTC), and the ACA.

- Medicaid changes include new work requirements for most non-disabled, non-elderly adults, mandating at least 80 hours of qualifying activities per month; restricting the use of provider taxes to draw down federal funding; tightening eligibility verification; lowering state financing flexibility; and introducing caps on state-directed payments. A new $50 billion rural hospital fund aims to offset the potential impacts.

- LTC changes include postponement of the federal staffing mandates for nursing homes; reductions in federal support for home- and community-based services; and changes in federal waivers, which could shift state investment strategies and affect LTC modeling assumptions.

- ACA changes include tightening subsidy eligibility verifications and eliminating the cap on excess advanced premium tax credit repayments; broadening the definition of plans that are eligible to use health savings accounts, regardless of traditional deductible thresholds. It’s important to note that the OBBA did not extend the enhanced advance premium tax credits that are set to expire in 2025.

On Aug. 22, the U.S. District Court for the District of Maryland issued a memorandum opinion in partial support of the plaintiffs in City of Columbus vs. Kennedy. The opinion stayed the implementation of certain provisions of the June 2025 Marketplace Integrity and Affordability Rule, including:

- The requirement that enrollees in fully subsidized exchange coverage who fail to timely submit an application for an updated eligibility determination be subject to a $5 monthly premium until such an application is submitted.

- The policy permitting issuers, subject to applicable state law, to decline to effectuate new coverage if a customer fails to pay premiums owed for prior coverage.

- The imposition of pre-enrollment eligibility verification requirements for all special enrollment periods.

- The imposition of a requirement that Exchanges verify a consumer’s annual household income when tax return data is unavailable.

- The changes to the de minimis ranges for actuarial value calculations.

The U.S. Supreme Court issued several high-profile health care-related decisions during the final weeks of its term:

- On June 27, the high court struck down a federal appeals court ruling, concluding that the appointment of members to the U.S. Preventive Services Task Force, which recommends what items and services must be covered without cost-sharing under the ACA’s preventive health services requirements, is constitutional. As part of the decision in Kennedy v. Braidwood Management, Inc., group health plans and health insurers must continue to provide timely first-dollar coverage of items and services that are recommended by the task force.

- On June 26, the court ruled in Medina v. Planned Parenthood that states are allowed to exclude Planned Parenthood affiliates from their Medicaid programs.

- On June 18, justices ruled in United States v. Skrmetti that Tennessee’s ban on gender-affirming medical care was legal, validating similar bans on access to hormone therapy and other gender-affirming health care for transgender people under 18 in more than two dozen states.

On June 25, the House Education and the Workforce Committee approved HR 2571, amending the Employee Retirement Income Security Act of 1974 (ERISA) to exclude certain medical stop-loss insurance obtained by some group health plan sponsors from the definition of health insurance coverage. It will next move to the House for consideration.

On May 12, President Trump signed an executive order focused on aligning prescription drug prices in the U.S. with those paid in other countries. The executive order seeks to build upon actions taken during the president’s first term by including Medicaid and Medicare.

State

Massachusetts Gov. Maura Healy signed S. 2543, enhancing protections for reproductive and gender-affirming health care services in the state by improving privacy for those seeking such services and limiting the influence of external jurisdictions on related legal matters.

Illinois Gov. JB Pritzker signed SB 175, requiring self-insured plans covering public sector workers in the state to cover post-mastectomy care, as well as Klinefelter syndrome testing.

Alaska Gov. Mike Dunleavy signed SB 132, outlining significant amendments to Alaska’s health insurance regulations, including a provision that requires health care insurers to offer non-network options during enrollment.

California Gov. Gavin Newsom signed AB 951, which states that individuals previously diagnosed with developmental and autism disorders will not be required to undergo a second diagnosis to maintain their treatment coverage, thereby reducing barriers to access.

Newsom also signed AB 116, establishing a Transgender, Gender Nonconforming, and Intersex Wellness and Equity Fund, which provides ongoing financial support for health care programs and an increase in financial eligibility standards for accessing medications to 600% of the federal poverty level.

Oregon Gov. Tina Kotek signed SB 822, which alters provider network regulations and telemedicine coverage within health benefit plans to ensure they are adequate in number, geographic distribution, and guarantee access to all covered services, including mental health and substance use disorder treatments.

Kotek also signed HB 3134, prohibiting insurers from requiring prior authorization for certain health care procedures identified during approved surgical procedures, provided specific conditions are met. And, she signed HB 2013, requiring health insurers set reimbursement rates for behavioral health treatment using the same methodology as for medical and surgical treatments.

Missouri Gov. Mike Parson signed SB 79, expanding telehealth services in the state, permitting physicians to treat the partners of those diagnosed with sexually transmitted infections even without an existing doctor/patient relationship, and creating a reimbursement structure for hospice care and rehabilitation services.

North Carolina Gov. Josh Stein signed SB 479, which requires pharmacy benefit managers (PBMs) to report to the Department of Insurance, establishes licensing and regulatory oversight of pharmacy services administrative organizations, and applies existing state regulations around prescription drug coverage to PBMs.

Stein also signed HB 546, which changes the state’s Medicaid program and health care reimbursement structures, impacting various sectors, including acute care and psychiatric hospitals. He also signed HB 357, which mandates continuing care communities obtain licenses and adhere to strict actuarial standards to ensure they can meet their financial obligations to residents.

Florida Gov. Ron DeSantis signed HB 677, mandating coverage for standard fertility preservation services within state group health insurance plans in Florida, particularly for those individuals undergoing cancer treatments that may result in infertility.

Pennsylvania Gov. Josh Shapiro signed SB 95, requiring pharmacists to disclose the retail price of prescription medications, the consumer’s cost-sharing amount, and relevant health coverage information upon request.

Rhode Island Gov. Dan McKee signed HB 5120, introducing a three-year pilot program that eliminates prior authorization requirements for certain services ordered by primary care providers.

McKee signed SB 114/HB 5634, which bars discriminatory actions by health insurers, PBMs, and pharmaceutical manufacturers concerning 340B covered entities and their contract pharmacies.

Maine Gov. Janet Mills signed SP 460/LD 1100, mandating that health carriers must approve prior authorization requests for nonformulary drugs used to treat serious mental health issues when formulary options are unavailable due to shortages.

Mills also signed LD 1580, prohibiting insurance carriers and PBMs from utilizing spread pricing in their operations, and LD 1310, requiring all group health plans outside the smallest to provide coverage without cost sharing for the first primary care and first behavioral health office visits each plan year.

Georgia Gov. Brian Kemp signed HB 422, requiring that state employee health plans offer at least two high-deductible health plans from different insurance providers, and that employees enrolled in such plans have the option to make pretax contributions to health savings accounts.

Connecticut Gov. Ned Lamont signed SB 10, establishing new requirements for health carriers concerning mental health and substance use disorder benefits, emphasizing compliance with state and federal reporting standards.

Texas Gov. Greg Abbott signed HB 3505, establishing and creating operational requirements for health care provider participation districts, intended to address the compensation of certain hospitals through a health care provider participation program.

Abbott also signed HB 541, establishing a framework for direct patient care agreements in the state, and HB 721, amending health care cost disclosures by health benefit plan issuers and administrators in the Texas Insurance Code.

Louisiana Gov. Jeff Landry signed HB 264, banning spread pricing and effective rate pricing by PBMs and requiring written notice to health insurance issuers and policyholders regarding any pricing practices.

Minnesota Gov. Tim Walz signed HF 2, focused on telehealth services regulations as well as creating new drug pricing and adjustments to Medicaid reimbursement rates regulations.

Vermont Gov. Phil Scott signed S 126, which focuses on the development of methodologies for payment reform, rate setting, and the establishment of reference-based pricing and global hospital budgets.

Nevada Gov. Joe Lombardo signed AB 428, mandating that public and private health plans, including Medicaid, provide coverage for fertility preservation procedures for individuals diagnosed with breast or ovarian cancer.

Lombardo also signed AB 511, which enhances reimbursement rights for various licensed healthcare professionals, including chiropractic physicians, acupuncturists, licensed psychologists, marriage and family therapists, clinical professional counselors, social workers, podiatrists, clinical alcohol and drug counselors, and registered nurses.

Lombardo also signed SB 389, requiring the Department of Health and Human Services to select and enter into a contract with a single state pharmacy benefit manager to manage coverage of prescription drugs under the State Plan for Medicaid, CHIP, and other health benefit plans that elect to use the Medicaid formulary by Jan. 1, 2030.

Colorado Gov. Jared Polis signed HB 25-1094, restricting PBMs to a flat-dollar service fee for their services, which must be clearly documented in agreements with health benefit plans.

Polis also signed SB 25-071, restricting pharmaceutical manufacturers, third-party logistics providers, and re-packagers from imposing limitations on 340B covered entities regarding the acquisition and delivery of 340B drugs.

Iowa Gov. Kim Reynolds signed HF 972, which creates a funding model for the rural health system, establishes a health care professional incentive program, and the Iowa health information network.