By Amarnath Suggu

Generative AI can boost efficiency in underwriting, claims, and IT, but overuse risks eroding judgment and empathy. A balanced framework ensures benefits without losing the human touch.

Many see generative artificial intelligence (GenAI) as a technological breakthrough with the potential to change the course of human civilization, largely because of its remarkable language capabilities. With the recent advances in agentic architecture, it has been heralded as a way to improve productivity of large enterprises by automating various business processes and reducing the need for human intervention. It’s no surprise that many enterprises, big and small, have rushed to adopt this technology.

GenAI is still in its early stages of evolution. It will take a while before we fully understand its advantages and drawbacks, especially its long-term effects on both people and the business world. Enterprises would be wise to keep this in mind and proceed with caution while recognizing the benefits of this technology.

The GenAI Dilemma

While it’s too early to understand its impact on socioeconomic systems and humans, researchers are aware of the many challenges, including technical and legal issues, that GenAI raises. It can hallucinate and generate misleading or incorrect information, and it reflects the biases present in its training data. In addition, if training data have not been procured through legal means, the generated content can potentially infringe on copyrights and other intellectual property rights. Early research indicates that the prolonged use of GenAI can impair the cognitive abilities[1] of humans, especially in knowledge acquisition, reasoning, learning, and creativity and critical thinking.

GenAI can automate many routine tasks, even some that require intelligence, in today’s business environment. As a result, its adoption may displace humans from existing roles, posing a challenge to the insurance industry. On one hand, the industry has an aging workforce and is unable to attract new talent.[2] On the other hand, it needs to effectively utilize the displaced employees, or risk losing both them and their valuable business knowledge.

This puts many organizations in a dilemma: whether to embrace the technology and reap its benefits, or resist and play safe. The choice largely depends on the leadership, the nature of the business (whether customer-centric or not), and the type of activities involved, including their criticality and complexity.

The GenAI Adoption Matrix

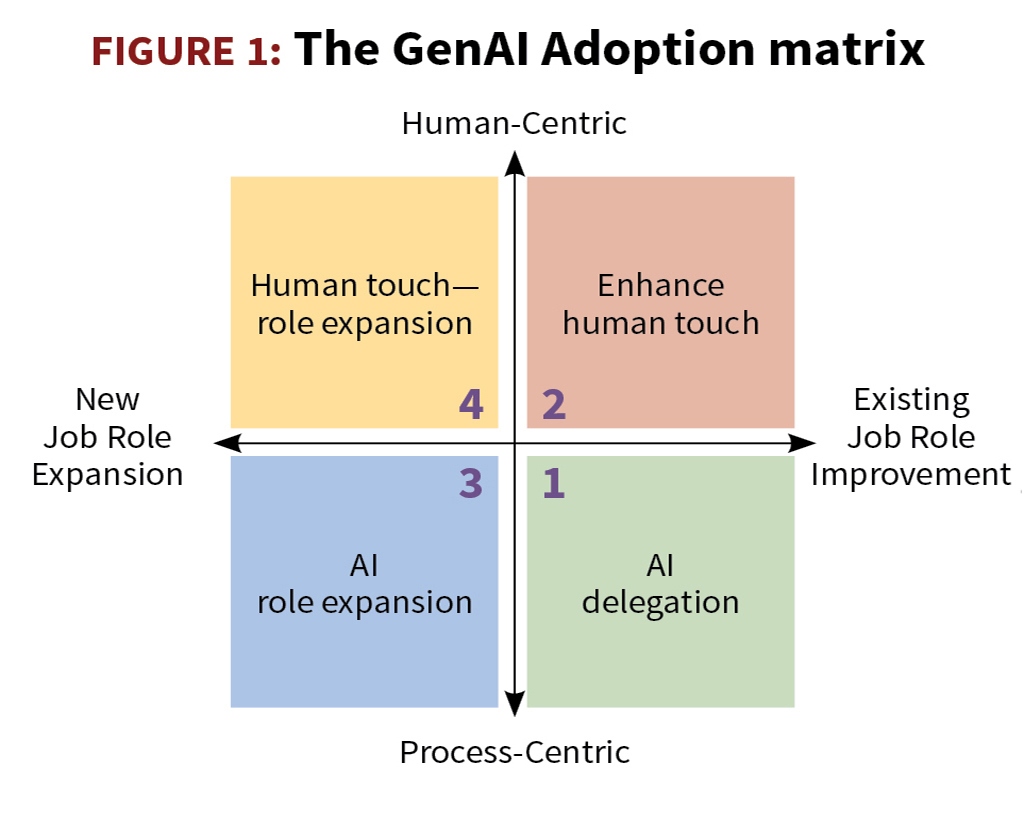

To overcome this dilemma, I propose a simple framework—the GenAI adoption matrix—which helps identify tasks in a business process best suited for GenAI deployment to maximize the benefit realization while limiting potential negative impacts. The framework is based on the premise that human emotions are essential for building customer relationships and tasks that do not require a human touch can be considered for automation. It also draws on research into strategies[3] employed by writing professionals to remain relevant in the GenAI age.

The GenAI adoption matrix consists of a horizontal and vertical axis that divides the plane into four quadrants (see Figure 1). The vertical axis denotes human-centric activities at the top and process-centric activities at the bottom. The right side of the horizontal axis denotes the current role performed by an individual, and the left denotes new or additional roles that can be performed by the same individual.

Human-centric activities, as the name says, are tasks that are better performed by humans. They include understanding customers’ needs and guiding them to choose a suitable product or showing empathy when the customer has lost a loved one or a valuable item. They also include critical tasks like judging people for financial eligibility, insurance coverage, or for criminal activities.

Process-centric activities, on the other hand, are a predefined set of instructions performed by a persona. These can be delegated either to another individual or to a machine. Examples include extracting information from documents, performing calculations, generating reports, and retrieving or updating data from various data sources.

Understanding the Adoption Matrix

The adoption matrix requires identifying the persona—whether an incumbent, a displaced subject matter expert, or a recruit—and the business tasks associated with the role, whether customer facing or routine activities. The recommendations generated by the matrix vary by persona for a given role.

Let’s apply the matrix to some of the scenarios described earlier to see how it works.

In the case of an individual performing the current role, the matrix makes two recommendations. First, embrace GenAI for repetitive tasks (quadrant 1) that result in process efficiency and improved customer satisfaction. Second, resist GenAI or limit its use to support activities that enhance and strengthen the human presence where it is essential (quadrant 2) to establish a customer connection and improve loyalty.

With the adoption of GenAI, an individual’s productivity increases, creating the bandwidth to take on more work or new role in some cases. In the new role, the individual can delegate new tasks to GenAI (quadrant 3—AI role expansion) and focus on new human-centric tasks (quadrant 4—human touch expansion) as the role demands.

It’s important to understand that delegating everything to AI is not sustainable in the long run as a lack of human touch in the business processes can adversely impact customer satisfaction and result in business loss. At the same time, humans who delegate work to AI should be held accountable for its output. This ensures that humans constantly monitor and review the AI systems and their output. In the process, they hone their reasoning and debugging skills which prevents cognitive skill impairment and other negative effects of AI. In the same vein, resisting AI and delegating all tasks to humans is also impractical, as it is not scalable. Hence, it’s essential for organizations to strike a balance between delegating tasks to humans and AI.

Applying the Adoption Matrix to Insurance

The insurance industry is a solicited business, unlike banking or retail/consumer goods, where products are sought by customers. Empathy and human touch are still important for advisors when selling policies and for adjusters when settling claims.

Let us consider a few business processes to identify areas where GenAI can be adopted using the matrix.

Talent management. The insurance industry is currently grappling with talent shortage issues. An aging workforce is approaching retirement and needs to be replaced, yet younger talent is reluctant to join, perceiving the industry as dull, boring, and not tech savvy.[4] This creates an ideal opportunity to embrace GenAI, which can attract new talent by offering the promise of working with emerging technologies. At the same time GenAI-based tools could act as a coach or assistant, reducing the learning curve as new talent transitions into roles previously held by existing staff.[5]

Sales and marketing. A sales agent or risk advisor occupies a highly customer-centric role, where establishing a genuine connection, earning trust and convincing customers are essential to conducting business. The human touch is critical and cannot be replaced by AI. Insurers have attempted to bypass agents through direct-to-consumer channels. However, except for a few lines such as personal auto and property, direct sales have not been successful.

Instead, insurers can support agents with product feature extraction and comparison tools, financial calculators and personalized marketing content generators to make their jobs easier. The sales personnel can utilize the additional bandwidth from AI delegation to strengthen their bond with the customers.

They can improve customer awareness on various product benefits and recommend coverages based on their needs. In the process, they can expand their roles to become advisors. This can result in additional sales and win customer loyalty.

Underwriting. Underwriters collect information from various third-party sources and review the information in detail to arrive at the risk profile. They ultimately decide whether to cover the risk or not, exercising their own discretion. GenAI can automate underwriters’ operational tasks, though not the decision-making itself. Automation opportunities include data extraction, guideline comparison, and premium calculation. With the increased productivity from AI automation, underwriters can expand their current roles to include new lines of business as part of their job.

Claims. A claim intimation or a first notice of loss (FNOL) call requires the handler to show empathy toward the insured’s loss whether it involves a disability, a human life, or a valuable item. The call is typically handled by an intermediary or a call center, where all the information is collected before handing it to a claim adjuster. While this task cannot be replaced by AI, the information capture can be supported by a bot. GenAI can automate most of the claim adjuster’s tasks, such as validating the claim information, estimating the loss, and determining the settlement amount. This can significantly increase the claim adjusters’ bandwidth for additional work.

A claim adjuster can enhance their customer interaction skills and expand the role to handle claim intimation calls. This will ensure that all the required information and clarifications are captured in a single call, improving the customer experience, especially in difficult times. At the same time, the claim adjuster can leverage composite AI to detect fraudulent claims and take up additional responsibility of a claim investigator as well.

Information Technology. GenAI can perform developers’ tasks such as drafting requirements, generating code, and creating test cases and test data. As a result, adopting GenAI in IT will increase team productivity and provide plenty of opportunities for role expansion. A business analyst can now leverage GenAI to draft requirements, allowing more time with business teams to elicit details. The analyst can also become a developer and create a Proof of Concept for new business functionality. A developer or a business analyst can play the role of a tester and improve code quality in the early stages of development.

A Balanced Approach

GenAI is a powerful technology that can take automation to new heights in the digital world. Embracing GenAI will improve process efficiency and employee productivity, leading to cost savings and customer satisfaction. But it comes at a cost. Extended exposure to this technology can make employees complacent and weaken their cognitive abilities. Excessive integration into every job and task, though cost effective, lacks the much-needed human touch in customer interactions.

Insurers can take a balanced approach to GenAI adoption. The matrix provides a good starting point to identify tasks where this technology is suitable and where it’s not. We should embrace it to automate the mundane tasks that boost overall efficiency and productivity. At the same time, we should resist its use in tasks requiring an emotional connection with customers. After all, our end customers in this business are humans, not machines.

AMARNATH SUGGU is a senior consultant at Tata Consultancy Services’ Insurance Business Unit.

Endnotes

- Protecting Human Cognition in the Age of AI; Cornell University; April 11, 2025.

- “Insurance Brain Drain: Tackling The Talent And Knowledge Crisis With AI”; Forbes; July 15, 2024.

- AI Rivalry as a Craft: How Resisting and Embracing Generative AI Are Reshaping the Writing Profession; [4] Cornell University; March 12, 2025.

- Insurance Industry Talent Crisis; AmTrust Financial.

- A fresh look at HCM through the GenAI lens; Tata Consultancy Service.

Academy Resources on AI

The Academy offers a wide range of articles, publications, and events focused on artificial intelligence (AI), including:

- “The Future Is Here”: A Contingencies article on how AI is transforming actuarial work.

- Actuarial Professionalism Considerations for Generative AI: A discussion paper on the use of AI and professionalism issues actuaries should consider.

- Discrimination: Considerations for Machine Learning, AI Models, and Underlying Data: An issue brief that defines discrimination; outlines methods for testing and monitoring algorithms; provides a regulatory overview; and highlights considerations for actuaries, model creators, and regulators. These publications are available on the Academy website at actuary.org.

- Analysis of NAIC AI/Machine Learning Surveys: A webinar examining how AI and machine learning are being adopted across the insurance industry, based on NAIC survey findings. Access it on Academy Learning (learning.actuary.org).