Click here for a print-ready PDF of this page. Read other articles in the Essential Elements series here. |

Plugging Holes in U.S. Flood Insurance

|

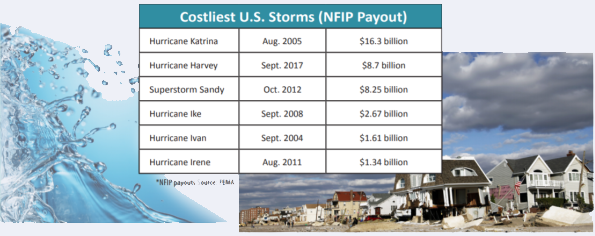

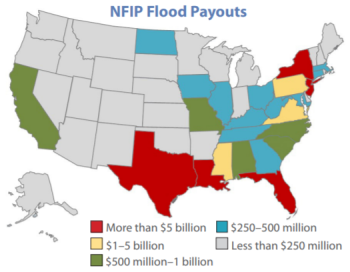

Flood insurance is vital to people and businesses that are located along the U.S. coastlines or major rivers and waterways throughout the country. But the costs of losses caused by flooding can also fall on American taxpayers who live outside of the path of destruction because of government actions or programs to deal with flood losses caused by major hurricanes and river flooding, which can destroy multitudes of homes and businesses in a single disaster. The National Flood Insurance Program (NFIP) was established in 1968 to provide flood insurance to homeowners, renters, and business owners in participating communities through collaboration between the federal government and private property insurance companies. The NFIP allows flood risks to be pooled on a nationwide basis so that the fund can theoretically absorb losses from periodic regional storms. The NFIP’s founding goals were to provide flood insurance, identify flood risks, and set minimum national building standards in flood zones and encourage communities to exceed those standards. As of December 2019, the NFIP had accumulated $20.5 billion in debt owed to the U.S. Treasury. (Official numbers for 2020 storms are not yet available.) Those funds were used to pay off insurance claims from catastrophic storms and floods over the past decade. Insurance premiums paid by property owners in flood-prone areas are not expected to be enough to both cover future insurance claims and retire the NFIP’s debt. Additionally, with rising sea levels and the likelihood of costlier storms, insurance premiums will continue to be insufficient to cover losses, and the NFIP’s debt may rise further without reforms to the program. However, raising flood insurance premiums too much too quickly could prompt homeowners and businesses to cancel their flood insurance policies or potentially to relocate to other parts of the country. In an effort to make the NFIP more financially stable, Congress passed the Biggert-Waters Flood Insurance Reform Act in 2012, which substantially cut subsidies on flood insurance that had been provided to some property owners, and extended the program’s authorization for five years, through September 2017. Congress later delayed some premium increases after concerns were voiced by policyholders. Congress has passed legislation authorizing 15 short-term extensions of the NFIP since 2017. The latest extension of the program is set to expire on Sept. 30, 2020, after which Congress must renew the program or risk flood insurance policy lapses. |

|

Steps to Address the NFIP Debt1. Revise financing of mega-storm lossesMost insurance systems have some plan for distributing losses from extreme events that include guaranty funds, catastrophe bonds, or government guarantees. Policymakers could rethink how the NFIP deals with losses from mega-storms like Hurricane Katrina, such as incorporating new private and public financing options.

2. Adjust insurance premiumsThe Casualty Practice Council of the American Academy of Actuaries believes charging actuarially appropriate premiums that reflect the hazards of better-defined categories of insured risks is good public policy. This could make the NFIP more financially stable on a long-term basis and more likely to be able to fully fund future losses. 3. Change policies on properties that report multiple flood lossesAbout 1% of NFIP-insured properties have accounted for more than 33% of the claims paid, according to one estimate. Owners of properties that have incurred multiple claims for flood damage could be required to pay higher insurance premiums. 4. Expand insurance coverageIf a higher percentage of property owners in participating communities within flood-prone regions bought flood insurance, the added revenue would be available to help pay off debt and future claims. 5. Improve flood mapsOver the past few years, the Federal Emergency Management Agency (FEMA) has been updating flood maps to provide more accurate information about flood risks. The sooner FEMA can finalize updated flood maps, the more quickly insurance premiums can be adjusted to more accurately reflect the flood risk of a specific property. 6. Shift private insurance companies into flood-insurance marketInsurers have started offering commercial multi-peril policies that include flood coverage, and residential coverage above the limits available from the NFIP. However, private insurance still comprises a very small portion of the market. Legislation has been proposed in Congress that would help expand the private marketplace and make coverage more widely available. |

|

Additional Resources from the American Academy of ActuariesThe National Flood Insurance Program: Challenges and Solutions (September 2019) Flood Insurance Private Coverage: Questions for Regulators (July 2018) |

|

1850 M Street NW • Suite 300 • Washington, DC 20036 • 202.223.8196 Copyright 2020 American Academy of Actuaries. All rights reserved |