by Jeyaraj (Jay) Vadiveloo and Karishma Gupta

Retirees face the challenge of balancing income security with investment growth. This article explores key factors influencing retirees’ need for guaranteed income and offers a framework to better understand how to optimize retirement spending while managing risk.

While every retiree is unique, they all want to use their fixed retirement assets to maximize their annual spending in retirement without running out of income before death. This is the safety-performance balance that every retiree seeks to optimize.

In our previous November 2023 Contingencies article, “Security, Safely—Evaluating the effectiveness of a combined investment-and-annuity strategy for retirement planning,” we introduced the SecureVest retirement planning model, which balances annuities with a risky investment portfolio to maximize retirement spending at a given ruin probability. Our model demonstrates that this integrated (i.e. guaranteed annuities plus investments) financial planning model can outperform a 100% risky investment strategy in many scenarios.

In the previous article, we assumed the retiree had a predetermined allocation of retirement assets in guaranteed investments based on individual preferences. In this article, we present a qualitative model to estimate this guaranteed allocation, drawing on several articles and studies about the various factors that determine the level of confidence a retiree has in the safety and security of their annual retirement income. The greater the level of confidence, the lesser the proportion of retirement assets allocated to guaranteed investments. We have quantified the various factors impacting safety and confidence into an index—the SecureRetireIndex (SRI)—inspired by our SecureVest retirement planning model.

Both SecureVest and SRI provide a carefully constructed methodology for how actuaries and insurers can demonstrate the value of incorporating guaranteed investments in retirement planning. Ultimately, that decision is in the hands of the retiree and their financial advisor, who could incorporate many more variables than those we consider in these articles.

The companion model, SecureVest, uses classic stochastic projections and actuarial assumptions to develop an optimal integrated retirement planning strategy for a predetermined level of guaranteed investments. The SRI builds on the SecureVest model to estimate the level of guaranteed investments needed. It uses a qualitative model to calculate the SRI.

Factors Impacting the Need for Safety and Security

There are several factors impacting the need for safety and security during retirement. Based on an extensive literature review and internet search, we narrowed down the following factors that contribute to a retiree’s need for safety and security.

- Dependents: If someone has financial dependents, they may prioritize having a guaranteed income to ensure that the support they provide to their dependents is consistent and stable.

- Social connectedness: The more socially connected a retiree is, the lesser the need for guaranteed investments, because there is a social network for the retiree to rely on.

- Health/longevity: If someone is in good health, there is a greater appeal to hold more guaranteed investments to protect against longevity risk.

- Lack of other income sources: The greater the availability of other sources of retirement income, the lesser the need for a guaranteed stream of income and dependence on stable retirement income.

- Influenced by level of education and skills to earn additional income during retirement

- Low tolerance to risk: Some retirees are more risk averse than others, preferring a more predictable and stable source of guaranteed income.

- Value simplicity: Some retirees dislike complex investment arrangements as they are harder to manage/understand.

- Influenced by the retiree’s level of financial literacy

- Discipline: Some people don’t trust themselves to manage overspending or withdrawing too much money from their investments, and prefer the stability of guaranteed income to keep them in check.

There could be other factors impacting the need for security at retirement, but these are the key considerations.

Calculating the SecureRetireIndex

To create a quantitative value from qualitative factors, we first developed an ordinal scale for these factors. We made the scale discrete with five values ranging from 1 to 5, where 1 represents the greatest need for retirement safety and 5 represents the lowest need for retirement safety. The scale for each of the factors is described below:

- Dependents: 1 = 4 or more dependents, 2 = 3 dependents, 3 = 2 dependents, 4 = 1 dependent, and 5 = no dependents

- Social connectedness: 1 = minimal social connectedness and the lack of a safety net, 2 = low social connectedness, 3 = average social connectedness, 4 = above-average social connectedness, and 5 = a high level of social connectedness

- State of health: 1 = excellent health, 2 = above-average health, 3 = average health, 4 = below-average health and 5 = poor health

- Availability of other income sources: 1 = no other sources of income, 2 = limited other sources of income, 3 = average other sources of income, 4 = above-average other sources of income, and 5 = several other sources of income

- Risk tolerance: 1 = highly risk averse, 2 = below-average risk tolerance, 3 = average risk tolerance, 4 = above-average risk tolerance, and 5 = high level of risk tolerance

- Value simplicity: 1 = a low level of financial literacy and need for investments that are easier to understand, 2 = below-average level, 3 = average level, 4 = above-average and 5 = a high level of financial literacy

- Discipline: 1 = a retiree with very little discipline in managing their investments and spending, 2 = low discipline, 3 = average discipline, 4 = above-average discipline, and 5 = a high level of discipline in financial management.

The next step in calculating the SRI is recognizing that all these factors are not equal in importance. We analyzed several sources to determine weights for these factors; links to these sources are provided at the end of the article. Based on our literature review, we assigned the following weights for each of the seven factors and calculated the weighted average for a given response:

- Other income sources–25%

- Health/longevity–20%

- Risk tolerance–15%

- Dependents–10%

- Discipline–10%

- Financial literacy/value simplicity–10%

- Social connectedness–10%

To construct the SRI, we use simple linear interpolation. We first determine the maximum weighted score if each response is 5 (i.e., the lowest need for retirement safety) and set this value to zero. We then determine the minimum weighted score if each response is 1 (i.e., the greatest need for retirement safety) and set this value to 100. We then interpolate between the minimum and maximum weighted scores for each given weighted outcome using the formula:

SRI = 100 × (max. score – given outcome) /

(max. score – min. score)

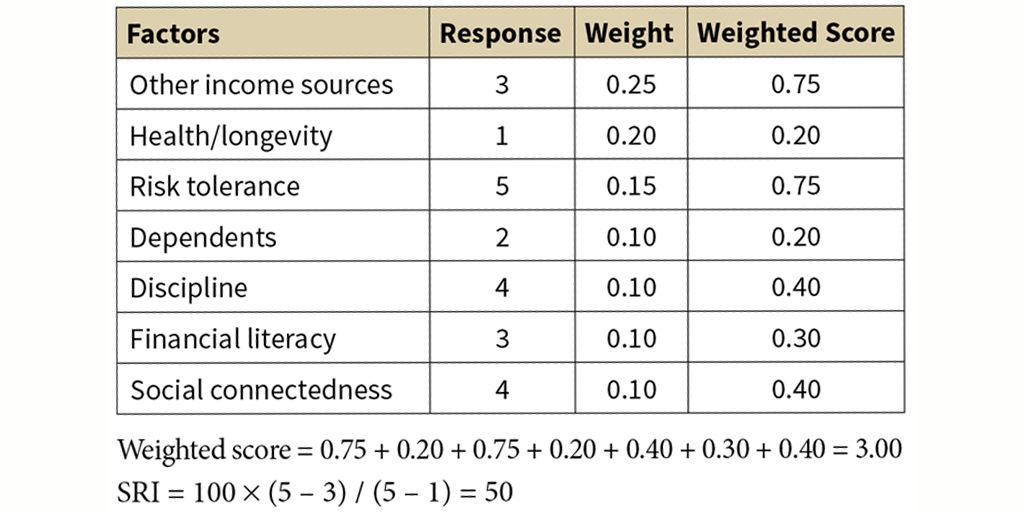

To illustrate, suppose we have the following responses for each of the seven factors:

Fac 1=3, Fac 2=1, Fac 3=5, Fac 4=2, Fac 5=4, Fac 6=3, Fac 7=4

Next Steps

To facilitate the SRI calculation, we have developed a simple Excel calculator that determines the SRI for a given response to the seven key factors impacting the level of safety and security a retiree may need at retirement. To access the calculator, visit the University of Connecticut Goldenson Center website and find the SRI calculator under their Projects tab.

The SRI can be used to estimate the desired percentage of investments that should be allocated to guaranteed investments in a retiree’s investment portfolio. Then we can use the SecureVest retirement planning tool to determine the optimal integrated investment strategy that maximizes annual spending for a given level of certainty.

The SRI can be generalized to include upper and lower bounds on the desired level of guaranteed investments. If we denote the lower bound as SRI(min) and the upper bound as SRI(max), then the SRI formula can be generalized to:

SRI = SRI(min) + (SRI(max) – SRI(min)) ×

(max. score – given outcome) / (max. score – min. score)

This article provides a novel qualitative approach to estimating the level of safety and security needed by a retiree. This approach is unique and, together with SecureVest, provides an actuarially sound framework to determine how retirement assets should be allocated between guaranteed and risky assets to maximize retirement spending for a given ruin probability. This framework could appeal to financial planners, actuaries, and annuity producers, and a financial planning app could be developed that combines the features of both SRI and SecureVest.

However, like all research on retirement planning, there are limitations to its practical application. There may be other criteria such as the need to leave behind a legacy or cover unexpected future expenses, that could influence a retirement planning strategy beyond safety and performance. Additionally, despite the rigorous analysis we conducted to determine the factors and weights influencing the need for safety at retirement, there is always an element of arbitrariness in any qualitative model.

To quote Jonathan Clements, “Retirement is like a long vacation in Las Vegas. The goal is to enjoy it to the fullest, but not so fully that you run out of money.”

Our SecureVest model, combined with the SRI calculator, customizes an investment strategy for a retiree that maximizes investment performance with a desired level of safety and security.

JEYARAJ (JAY) VADIVELOO is professor and director of the Goldenson Center for Actuarial Research at the University of Connecticut.

KARISHMA GUPTA is a junior majoring in Bioengineering at The University of Pennsylvania, with minors in Computer Science and Engineering Entrepreneurship.

Sources for Factors

- “Buying an Annuity”; Annuity.org; March 3, 2025.

- “5 Key Factors That Affect Annuity Rates (And How to Use Them to Your Advantage)”; The Annuity Expert.

- “How Behavioral Factors Shape Retirement Wealth; Knowledge at Wharton”; July 15, 2024.

- “How to feel financially secure in retirement”; Fidelity Viewpoints; July 9, 2025.

- “What Is a Single Life Annuity?”; PlanEasy; Nov. 6, 2024.

- “Pros and cons of annuities that experts say to know now”; Money Watch; May 19, 2025.

- “Structured Annuities and Settlements: Maximizing Financial Stability With Market Protection”; National Debt Relief; April 17, 2025.

- “Individuals’ challenges managing pensions through retirement”; The Pensions Review; April 1, 2025.

- “Annuity beneficiary payout options: What happens to my annuity when I die?”; Thrivent; May 13, 2025.

Sources for Weights

- “Coping with the Stress of Retirement”; Harvard Business Review; May 5, 2024.

- “Annuities: Whose Cup of Tea?”; Retirement Income Institute; December 2020.

- “Pension Plan Distributions: The Importance of Financial Literacy”; Pension Research Council; Aug. 24, 2011.

- “Time Inconsistent Preferences and the Annuitization Decision”; Journal of Economic Behavior and Organization; Sept. 10, 2016.

- “Annuitization Puzzles; Journal of Economic Perspectives”; Fall 2011.

- “Security, Safely—Evaluating the effectiveness of a combined investment-and-annuity strategy for retirement planning”; Contingencies; Nov. 1, 2023.